Duke University

is a hedge fund with a health system, a huge research enterprise & a hobby of college

Reforming higher education requires changing the incentives at play—for students, professors, presidents, alums and trustees. This post provides an overview of the economic model of Duke University, where I have been a professor since 1997 and played a variety of leadership and faculty governance roles. The modern research university is an exceedingly opaque organization and this piece begins to bring some clarity about the finances that drive the university incentive structure.

Is Duke Rich or Not?

The answer is yes, and no. There are only 10 to 15 universities in the U.S. that do not covet Duke’s financial resources—our problem is that we aim to compete with the very few who have far more money than Duke (e.g., Stanford, Harvard, Yale). This reality leads to the following repetitive conversation:

“How can Duke not afford to [ ] because we have Billions of dollars?” (exasperated tone)

The ‘cause’ in the blank might be a further increase in Duke’s minimum wage; expanding need-based financial aid for undergraduates, or extending same to international students; increasing the guaranteed stipend for Ph.D. students; or hiring more faculty in Physics. Or English. Or African and African American Studies. Or building more and better athletics facilities.

And on and on. The problem is that you can only spend a dollar once.

Duke could do most anything it wants to do, just not all of the things that it would like to do. Or that the loudest voices insist be done. And there are some financial problems that are baffling. For example, how Duke can have so much, yet today faces a multi-million dollar deferred maintenance problem that must finally be addressed?

How indeed? Numerous leaders responded to incentives over multiple decades leading to decisions to invest in new and exciting academic programs as Duke rose in prominence in the 1980s and 1990s. It was easy to prioritize such investments over modernizing the plumbing in classroom buildings. Duke is one of only six universities to have been ranked in the U.S. News and World Report top ten each time the list has been produced since the late 1980s, and leaders in the past 25 years have been risk averse to a potential Duke decline in standing on their watch. And creating new programs is how academic leaders get noticed and rise to loftier positions at other Universities, leaving someone else to worry about the toilets later.

Show Me The Money

Duke had net assets of $22.6 Billion at the end of fiscal year 2024, according to Duke Public Financial Statement 2023-24 (see figure below, from p. 4: Net assets of the University, including the School of Medicine, were $16.6B; Net assets for Duke University Health System (DUHS), were $6.0B). DUHS is a North Carolina based non-profit corporation that is a “wholly controlled affiliate of Duke University” (see note 1, p. 20). DUHS owns hospitals, physician practices in Durham and across North Carolina and a medical malpractice insurance corporation domiciled in Bermuda. Duke University owns the Duke Health System. When the Board of Trustees talk about Duke, they are likely referring to the University and the Health System.

I am working on a book project Renewing the marketplace of ideas on elite campuses and that work focuses on the last seven years at Duke University. The incentives at work in the University have great effect on any menu of reforms, and the remainder of this piece highlights three key financial takeaways that must be understood if one hopes to change the intellectual culture of Duke University.

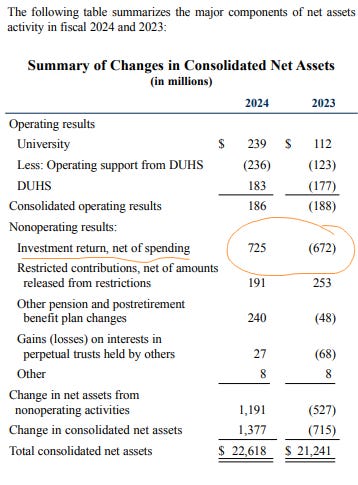

Investment Returns are Vital for Duke’s functioning. The table below (p. 4) demonstrates the importance of investment returns for Duke University operations (see circled; (672) means loss/negative return). In 2023, Duke spent $672 Million more than our combined net investments returned, while in 2024 we earned $725 Million more on investments than we spent. That is a difference from one year to the next of nearly $1.4 Billion.

The transition from 2023 to 2024 was unusual because the Duke University Health System bought the for-profit corporation physician practice (the Private Diagnostic Clinic) that has been a provider of physician services to patients seeking care at Duke since 1931. More on this odd and crucial part of Duke’s history later. The point is that Duke’s ability to function and invest in either maintenance or new programs is highly dependent upon the investment returns that Duke’s investment company DUMAC produces year to year. Further, the performance of the Duke University Health System has an effect on the financial bottom line of Duke University.

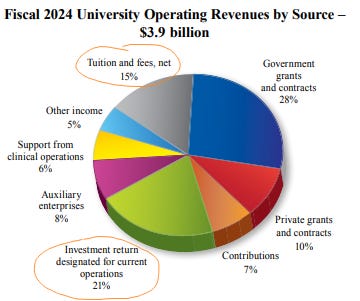

Research Grants are a key source of revenue and a huge part of what Duke University does. The annual operating revenue for the year July 1, 2023 to June 30, 2024 for Duke University was $3.9 Billion (figure below from same 2024 Financial Statement). The figure shows revenue sources of all ten Duke University Schools, including the School of Medicine. The schools ordered alphabetically: Business, Divinity, Engineering, Environment, Graduate School, Law, Medicine, Nursing, Public Policy, and Trinity (Arts and Sciences). The annual budget of each school varies greatly (more than 10x from School of Medicine to Divinity).

A few points to highlight.

Research grants and contracts represent ~ 4 in 10 University dollars; the U.S. federal government provided approximately $1 Billion, with private foundations $410 Million. The School of Medicine alone had just over $1.1 Billion in total research grant funding that year

Investment returns are a larger source of Duke University revenue (21% v. 15%) than tuition (net of financial aid)

Support from clinical (Health System) operations are a key cross subsidy of the University; the Health System is best viewed as an asset that has generated positive flows for most of the past 25 years; its performance moving forward will greatly affect Duke University

Where are football and basketball? Athletics is part of the 8% Auxiliary (see p. 23) enterprises, comingled here with residence halls, student dining, and parking. Neither the Duke Financial statement, nor the annual report of Duke Athletics contains budget information, but the Duke Chronicle reported the 2022-23 Athletic budget to be $150.5 Million in expenses against $152.5 Million in revenue. On net, the financial result is trivial, though the cross subsidies within Duke will be highlighted in later pieces, and of course athletics garners a great deal of attention.

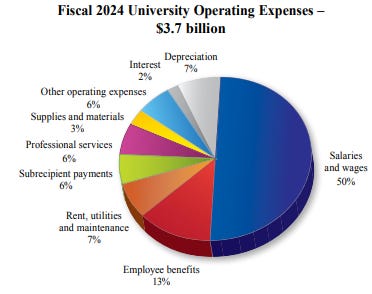

Nearly two-thirds (63%) of Duke’s operating expenses are salaries and benefits. The figure below breaks down the other categories. Most are self-explanatory, but subrecipient payments are most commonly research subcontracts where a Duke Faculty member who obtained a (usually) federal research grant chose to ‘purchase’ expertise from outside of Duke.

Like most organizations, if you want to undertake budget reductions in any area that means people losing their jobs, and that is exceedingly difficult.

I will return again and again to the incentive structure that is created by Duke’s financial model.

A good joke to understanding universities is that a STEM professor is half-way between a government contractor and an Amway distributor. To do research, the primary investigator needs a grant that functions much like a government contract. But with a grant, the primary investigator can hire others who can also apply for grants. At the highest levels, primary investigators are really just grants/contract managers. The third part of the joke is that the researcher has to kick up a significant portion of the grant to the bosses of the university to make sure everyone is taken care of.

What a gargantuan undertaking, Don!